Term vs. Whole Life Insurance: Learn the Difference Here Before Making a Critical Life Decision

Choosing between term and whole life insurance isn’t just about price—it’s about your goals, your family, and the legacy you want to leave. But if you’ve ever felt confused by the differences, you’re not alone.

This guide will break it down in plain English. You’ll walk away knowing:

- What each type of insurance really means

- How the costs compare (with real numbers)

Which one makes sense for you - And how to get a quote with no pressure

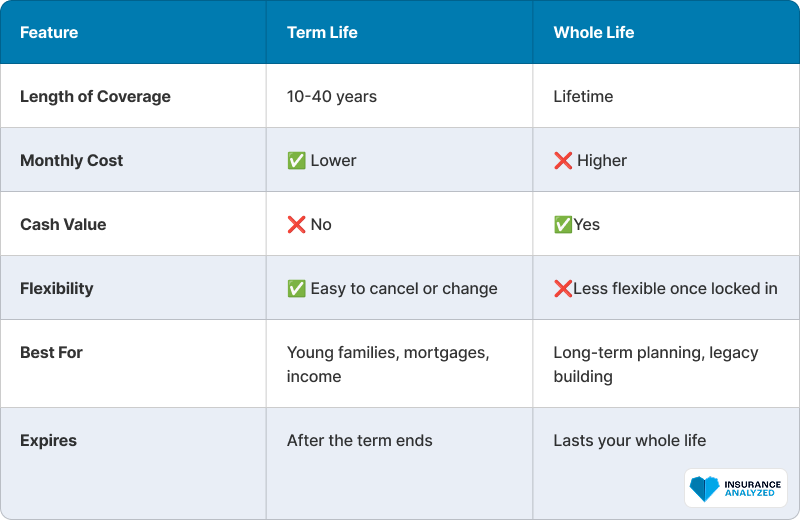

Term Life: Simple, Affordable, Flexible

Term life is the most straightforward kind of life insurance.

You pick a time period (or “term”)—say 20 years—and if you pass away during that time, your loved ones get a payout (called the death benefit). If you outlive the term, the policy ends.

Key Benefits

- Lower monthly premium

- Easy to understand

- Good for covering temporary needs (mortgage, raising kids)

Downsides

- No payout if you outlive the term

- Doesn’t build cash value

Here is a simple example. Ashley is a 30 years old, non-smoker. She Wants to protect her 2 kids until they’re grown:

- She would gets a 20-year term life policy

- Her coverage amount: $500,000

- Here monthly premium: $25/month

If Ashley passes away during that 20-year period, her kids get $500,000. If she’s still healthy and alive at 50, the policy ends—and that’s it.

Whole Life: Coverage for Life + a Savings Account

Whole life insurance is a type of permanent insurance. It covers you for your entire life—and it includes a built-in savings account (called cash value) that grows over time.

Key Benefits

- Coverage that never expires

- Builds cash value you can borrow from or withdraw

- Can be part of a long-term wealth plan

Downsides

- Higher monthly premiums (up to 10x higher than term)

- More complex to understand

- Less flexibility to adjust later

Here is a simple example. David is a 30 year old, non-smoker:

- Gets a whole life policy

- Coverage: $500,000

- His monthly premium: $280/month

David pays more than Ashley, but part of that money grows in a savings-like account. After 10–15 years, he can borrow against it, withdraw some, or leave it untouched to keep growing.

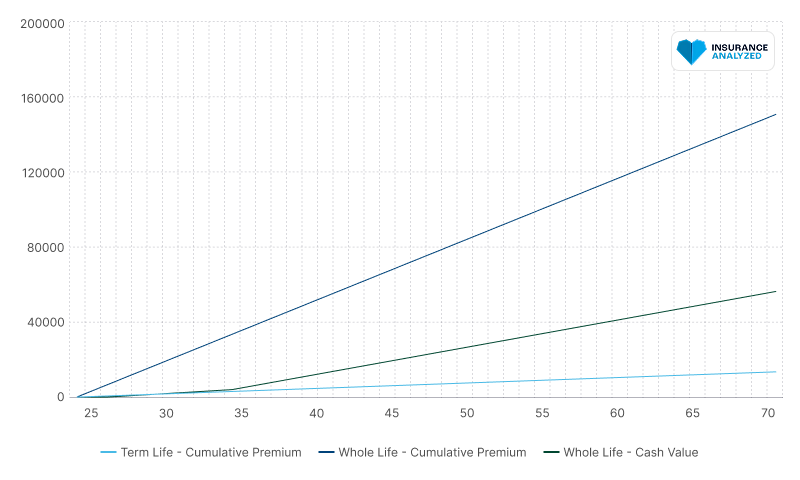

Side-by-Side Comparison: Term vs Whole

Lifetime Cost Comparison

This chart shows how term life costs stay low and fixed for 20 years, while whole life continues building costs (and value) for decades:

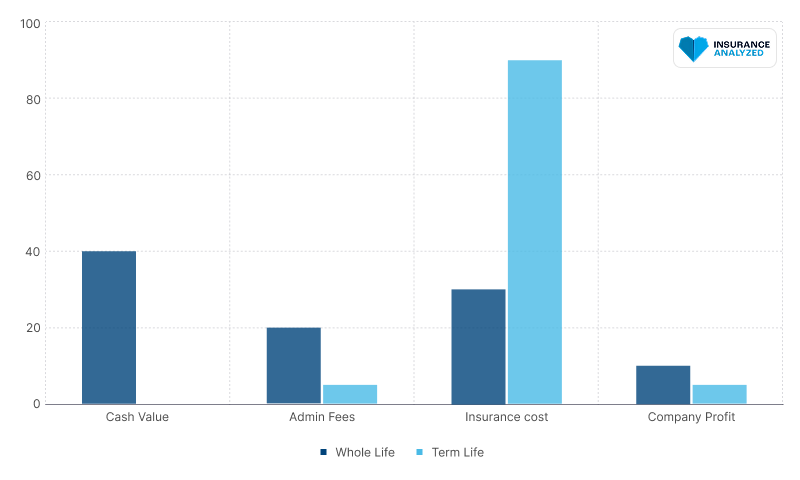

Where Your Premium Goes (Whole Life)

Do wonder why whole life costs more? Here’s how your premium is split:

Final Thoughts

There’s no one-size-fits-all answer. The key difference?

- Term life is like renting coverage when you need it most.

- Whole life is like owning a home—it builds value, costs more, but lasts forever.

Knowing which one fits your life stage and goals is the first step. And we’re here to help you find the right fit.

Common Questions

“What happens if I cancel my term policy?”

You stop paying, and coverage ends. There’s no refund—but no penalty either.

“Can I convert my term policy to whole life?”

Many policies allow you to convert within the first 5–10 years. It’s a good way to “test drive” life insurance.

“Does whole life make more sense for older adults?”

It can, especially if you’re focused on legacy planning or final expense coverage. But it’s more expensive the later you buy.